Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

After months of speculation about Argentina’s currency regime, we finally have an answer: no change. Will the bands be eliminated? No. The exchange policy remains intact, and the pressure on the peso has eased.

Before the election every newspaper and media were speculating about the eventual abandonment of an “obviously” unsustainable monetary policy. But keep in mind, as Javier Milei likes to remind us, “We do not hate journalists enough.”

Many take that as an attack on their profession. It isn’t. It’s an indictment of how journalism has decayed.

Too often, the media echoes (or repeats) rather than inquires, filters rather than clarifies. Whether from laziness, ideological bias, undisclosed interests, or sheer ignorance, the result is the same: noise disguised as journalism.

The tragedy is not just that “independent” journalists are in fact partisan; it’s that they mislead.

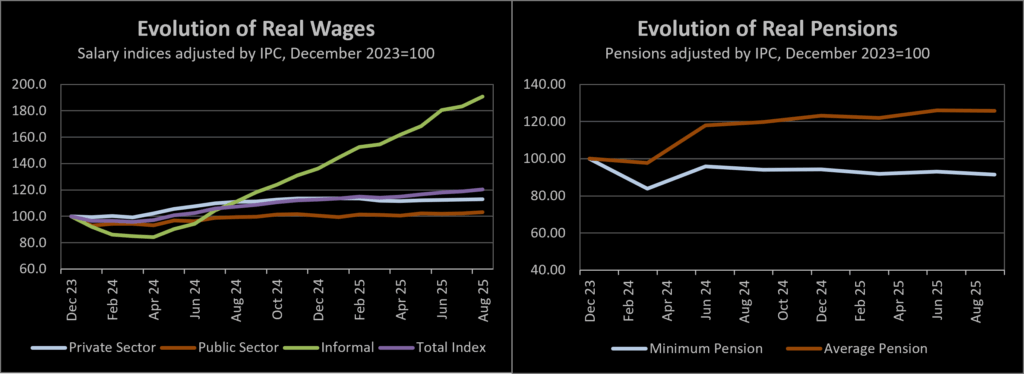

The Financial Times can claim with impunity that “Argentines are frustrated […] as wages and pensions fall in real terms due to austerity.” The reality? The opposite is true. Wages and pensions have risen in real terms.

Source: Chainsawnomics based on INDEC and Ministerio de Capital Humano.

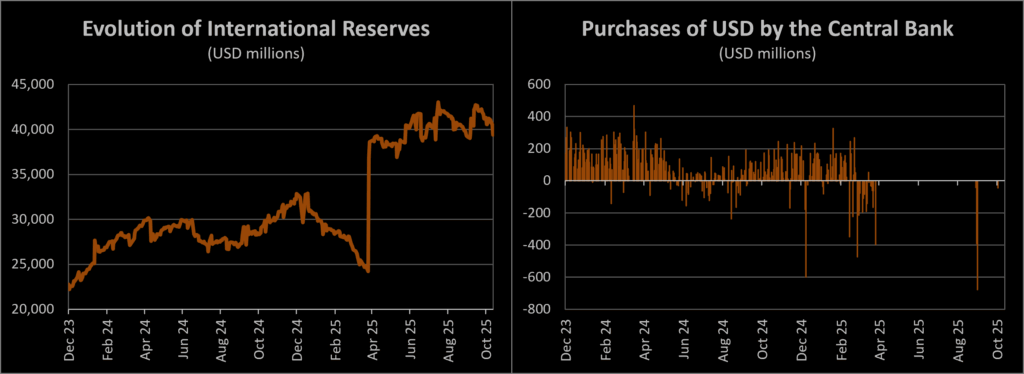

In the Lex column, they can write without blushing that peso was “overvalued,” making imports “artificially cheap” while “incinerating foreign reserves.”

In truth, Argentina’s protectionist structure keeps import prices artificially high. Exports are at record levels. And the Central Bank’s reserves have been stable. The FT’s readers would be surprised to hear that the total Central Bank interventions through selling of US dollar reserves since April was a modest $1.2 billion. Cetral Bank reserves stay at around $40 billion compared to a monetary base equivalent to $28 billion, which is less than 5% of GDP. That’s it.

The examples multiply.

Source: Chainsawnomics based on Banco Central de la Republica Argentina

The Myth of the “Free Float”

For the commentariat, the solution is always simple:

(a) Let the currency float.

(b) Accumulate reserves.

They say both in the same breath.

Yet a floating currency needs no reserves to defend it. The contradiction reveals the real intent: a forced devaluation to benefit Argentina’s protected industrial elites — the remnants of what might we call the Corporatist Republic, that Milei is dismantling.

What the “Crisis” Was Really About

Was this a fiscal crisis? No — Milei balanced the budget in his first month.

A debt crisis? Hardly — debt-to-GDP has fallen from roughly 156% to 61% since 2023.

Was the Central Bank financing the government? No.

The panic was political: fear of Peronism’s return. That fear drove a temporary flight from pesos, widened spreads, and knocked equities. When the risk subsided, so did the turmoil.

The Real Challenge: Credibility

Argentina’s issue is not solvency but trust. After decades of default and deceit, investors demand proof of permanence.

Fiscal discipline has been restored, nominal debt reduced by 10%, and total public spending cut by about 7 percentage points of GDP at the Federal level in two years (over 10 points when including the provinces). An astonishing adjustment. And to be clear, GDP grew during this period by over 3%.

If sustained, debt-to-GDP could fall below 30% by 2031, even to 20%. The plan is coherent. What it lacks is time, and a bridge of confidence.

This is where the US Treasury and IMF enter the picture: extending a swap line and exploring what sounds like a “neo-Brady” financing structure yet to be announced. If executed, this could anchor Argentina’s debt market access for the first time in over 50 years.

The Peso’s Future

Exports are expected to more than double by 2030. Energy, mining, and infrastructure investment is surging. With deregulation, productivity gains, and lower taxes, competitiveness will rise, and so will demand for pesos.

The irony is that Argentina’s next problem may be appreciation, not devaluation.

Will the government let the peso float? Yes, within the managed bands. But history suggests that when the market turns, those now demanding a “free float” will be the first to beg for intervention.

Risks and Reality Checks

Even so, Milei’s revolution is not irreversible. Argentina has rarely sustained reform beyond a single administration. Political fatigue, entrenched unions, or a divided Congress could still derail progress. The libertarian experiment’s success will depend on whether the country’s new generation, not its political class, insists on seeing it through.

Welcome to Argentina 5.0, a country where the war between freedom and the state is being fought in the open.